A gentle introduction to bitcoin

This article is a gentle introduction to bitcoin and assumes minimal technical knowledge.

Shorter companion pieces to this are:

- Bitcoin’s network in one infographic

- Inside bitcoin’s blockchain (infographic)

- A gentle introduction to bitcoin mining

In the popular media, you will often read comments like “Bitcoins are stored in a digital wallet”, or “You can send money using blockchain technology”. These comments can be misleading and can confuse. By the end of this you should understand enough to participate in a dinnertime conversation about bitcoin, and not be mystified by the topic.

Bitcoin

Although people refer to bitcoin as a decentralised digital currency, I prefer to think of it as an electronic asset, to sidestep questions around which government backs it and who sets the interest rate, which are often a mental block in understanding bitcoin.

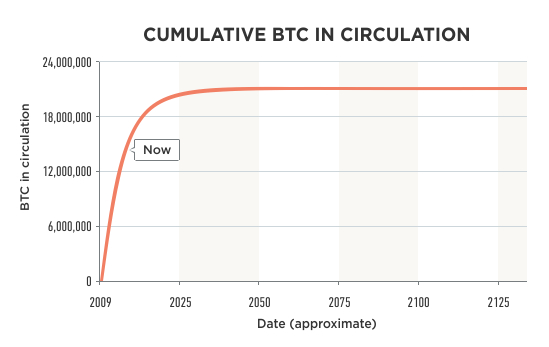

As an electronic asset, you can buy bitcoins, own them, and send them to someone else. Currently (Sep 2015) there are around 14 million bitcoins that have been created, increasing by 25 bitcoins every 10 minutes or so, with an agreed limit of 21 million, the last of which should be created a little before the year 2140.

Transactions of bitcoins from account to account are recognised globally in a matter of seconds, and can be considered securely settled within an hour, usually. They have a price (usually in USD, but can be against any currency, as with anything else), and the price is set by normal supply and demand market forces in marketplaces where traders come to trade, just like with oil or gold.

What is bitcoin designed for?

A 2008 whitepaper written by the pseudonymous Satoshi Nakamoto introduced the concept of bitcoin, and the design principle behind bitcoin is:

A purely peer-to-peer version of electronic cash [which] would allow online payments to be sent directly from one party to another without going through a financial institution.

So, there is the concept of electronic cash: cash being a bearer asset, like the cash in your pocket which you can spend at will without asking permission from a third party.

Before Bitcoin there was never electronic cash; we had numbers being stored in the database of a financial institution like a bank or Paypal, whose rules you had to comply with in order to open an account and use, and whose permission you had to seek before being able to move the money.

Why use Bitcoin?

I think of bitcoin like just another international currency whose ‘home ground’ is the internet, as opposed to any geographical location. Put another way: if the internet were a country, bitcoin would be its currency. For the first time we have an entirely digital asset which can be controlled by the end user, without requiring signup with an institution.

Bitcoin payments. Payments of bitcoins can be made from one person to another, irrespective of geographical location or jurisdiction. Payments are relatively fast – the initial notification is within seconds, and it ‘settles’ in about an hour. In situations where the normal financial system is inadequate, it can be a useful way of transferring value to anyone who has access to the internet.

Potential users. Some communities are underserved by banks due to the cost/benefit of the brick & mortar banking model and regulatory cost; some international transfers are unreliable, or can take many days, with manual processes and faxes being used as part of the plumbing; some people may want to accept digital money for selling digital goods; there may be use cases where small payments, in the order of pennies, may be useful, which is currently difficult with existing fee structures with credit cards. There may be other uses which we haven’t discovered yet…

Price volatility. Just like other currencies, bitcoin’s price fluctuates. Bitcoin’s price is more volatile than a lot of currencies (though the volatility is decreasing), so if you account for your wealth in your local currency, then owning bitcoin is essentially a bet on bitcoin’s future exchange rate price. You can see historical price volatility on Tradeblock’s website.

Conversion. Just like other currencies, if you have one currency (say, Pound Sterling), and you want to convert it to bitcoin, you need to find someone to exchange it with. This necessarily has some friction and fees: either dressed up as commissions; or built into the spreads (the conversion price). With time, conversion is getting easier and cheaper as more exchanges are springing up in more countries.

Maintain cynicism. You may hear of bitcoin being ‘fast’ and ‘free’ or ‘low cost’. While that is true when you are strictly in bitcoin, it’s worth maintaining some cynicism and thinking about the costs involved in the ‘on’ and ‘off’ ramp getting from sovereign currencies into bitcoin and back.

While I can’t imagine “mass consumer adoption” of bitcoin, I can imagine a group of freelancer developers or graphic designers in an emerging economy, who may not have access to banks or Paypal. With bitcoin, for the first time, they can do ‘digital’ work and be paid digitally. Of course, there is still the question of how they can convert bitcoin back into local currency, but that’s an easier problem to solve then receiving the money in the first place.

It’s worth noting that while bitcoin has spawned many other similar cryptocurrencies such as litecoin, dogecoin, bitcoin is still the most widely used and traded due to its network effect and relatively higher levels of security and robustness.

How does it work?

A network of computers validates and keeps track of bitcoin payments, and ensures that they are recorded by being added to an ever-growing list of all the bitcoin payments that have been made.

Keeping track of payments: The Bitcoin Blockchain

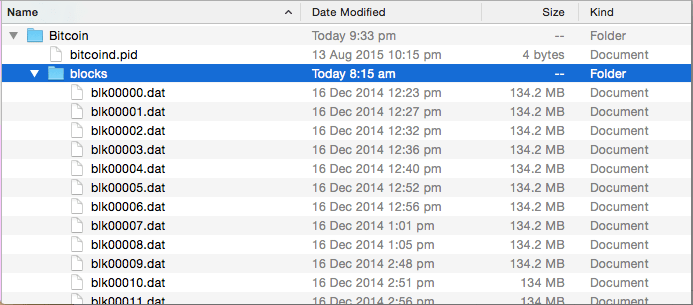

There is a file (well, split into several files) called “The Bitcoin Blockchain”, sitting on thousands of computers across the world, including my laptop at home. When you read the word “blockchain”, think “database” or even “list” and you have the right kind of idea. For a primer on blockchain please see A gentle introduction to blockchain technology.

A screenshot of The Bitcoin Blockchain files on my computer. Here you can see The Bitcoin Blockchain split into files, each 134MB big, and the total is about 50GB at time of writing.

This file contains data about all the bitcoin transactions, that is payments of bitcoins from one account to another, that have ever happened. This is often called a ledger, similar to a bank’s ledger which keeps a record of payments between bank accounts.

Simplified bank ledger vs bitcoin ledger: they are similar.

The bitcoin network. The computers which store this file also run software that connects them over the internet to the other computers running the same software. This forms a network of computers that can talk to each other, relaying information about

- new payments (at time of writing there is about one new bitcoin payment per second, but this comes in fits and starts)

- updates to The Bitcoin Blockchain (every 10 mins or so, a new “page” or block of valid transactions is confirmed and is distributed to all of the computers on the network)

When you make a bitcoin payment, a payment instruction is sent to the network. The computers on the network validate the instruction and relay it to the other computers. After some time has passed, the payment gets included in one of the block updates, and is added to The Bitcoin Blockchain file on all the computers across the network.

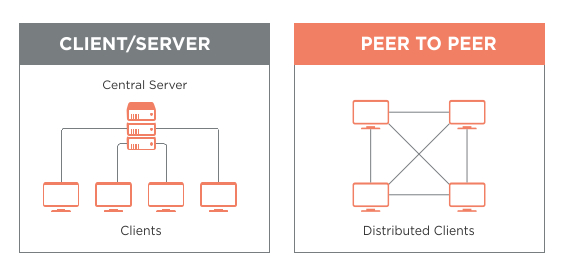

Peer-to-peer. The distribution of data works on a peer-to-peer basis, rather than client-server. Peer-to-peer is like a gossip network where everyone tells a few other people the news (about new transactions and new blocks), and eventually the message gets to everyone in the network. This is as opposed to client-server is more like a conventional organisation where a boss tells subordinates the news, and the boss is a central point of reference, and potential failure.

Client-server vs Peer-to-peer data distribution models

One benefit of peer-to-peer (p2p) over client-server is that with p2p, the network doesn’t rely on one central point of control which can fail.

How are bitcoins stored?

Bitcoin ownership is tracked on The Bitcoin Blockchain, and bitcoins are associated with “bitcoin addresses”. Bitcoins themselves are not stored; but rather the keys or passwords needed to make payments are stored, in “wallets” which are apps that manage the addresses, keys, balances, and payments.

Bitcoin accounts: addresses

In banking you have accounts which keep pots of money separate; in bitcoin you have addresses. A bitcoin address is similar to a bank account number, with a few differences.

Here’s an example of a bitcoin address: 1MKe24pNsLmFYk9mJd1dXHkKj9h5YhoEey. Just like with bank accounts, if you want to receive a bitcoin payment, you need to tell someone your bitcoin address, so they know where to send bitcoins to. A typical conversation, which could be in person, or online, or on chat (Whatsapp/Skype etc) looks like:

(BTC and XBT mean the same thing and are industry standard abbreviations for bitcoins, like GBP for Pound Sterling)

Bitcoin wallets

With my bank, under one single username/password, I control a number of accounts (eg incoming salary, monthly savings, tax, etc), each of which have a balance or amount of currency. Similarly, Bitcoin wallets are apps that display all of your bitcoin addresses, display balances and make it easy to send and receive payments.

For a wallet to provide accurate information, it needs to be online or connected to a Bitcoin Blockchain file, which it uses as its source of information. The wallet will read the Bitcoin Blockchain file and calculate the balances in each address.

Bitcoin wallets let you create bitcoin addresses to receive incoming transactions and make outgoing payments, plus have other features that make them user friendly.

How are bitcoins sent?

Payments, or bitcoin transactions

Each bitcoin address has its own private key, which is needed to send payments from that address. You can think of a key as a kind of password, but it’s mathematically linked to its respective address, so it can’t be changed, unlike a conventional password or PIN number.

For the address above (1MKe24pNsLmFYk9mJd1dXHkKj9h5YhoEey), the private key is 5KkKR3VAjjPbHPzi3pWEHVQWrVa3C4fwD4PjR9wWgSV2D3kdmeM. Whoever knows this private key, including readers of this blog, can now make payments from the address.

To get your own address/private key combination, it is not given to you by some authority like a bank, but rather you pick a random number and apply some maths to it – wallet software will do this for you.

Private keys. The private key is something you want to keep securely and never expose. Because you can not change that private key to something more memorable, it can be a pain to remember. Most wallet apps will encrypt that key with a password that you choose. Later, when you want to make a payment, you just need to remember your password.

Because bitcoins don’t exist as such, bitcoin wallets don’t store bitcoins but store the keys that let you transfer or ‘spend’ them. Copying a wallet doesn’t double the number of bitcoins you own, you simply have a copy of the same keys. If someone manages to copy and read your wallet, they can empty the accounts, just as two people with duplicate keys to a bank’s safe deposit locker can race to unlock the locker, but the contents of the locker do not double.

Bitcoin wallets contain private keys, not bitcoins!

What happens when I make a bitcoin payment?

A payment is an instruction to unlink some bitcoins from an address you control, and move them to the control of another address (your recipient).

Your payment instruction includes everything you’d expect, including:

- which bitcoins you’re sending

- which address you’re sending them from

- which address you’re sending them to

Digital cryptographic signatures. The instruction is then digitally signed with the private key of the address which currently holds the bitcoins. This digital signing demonstrates that you are owner of the address in question (because only you know the private key).

Payment instructions are sent from the wallet software to any of the computers on the network (called “nodes” or “payment validators”).

Validators. When the first computer receives the instruction, it checks some technical details, and some business logic details (eg, does my payment attempt to create bitcoins out of nothing? Have the coins being sent already been sent elsewhere? etc).

Validators validate at technical and business logic levels.

If these tests pass, then the computer relays it to others on the network, who each run the same validation tests. Remember on this network, computers can’t trust each other so they have to run the same tests. Eventually all computers on the network know about this payment, and it appears on screens everywhere in the world as an “unconfirmed transaction”. It is unconfirmed because although the payment has been verified and passed around, it isn’t entered into the ledger yet.

How are bitcoins tracked?

How do transactions get entered into everyone’s blockchains?

As well as passing information about transactions between each other, specialised nodes (computers who form part of the network) work to add these transactions, in blocks, to the blockchain. This is known as “mining” bitcoin. This is often described as “solving complex mathematical puzzles to win bitcoin”. In fact there is nothing complex about this process, and you can do this by hand without a calculator; it just deliberately takes many computational steps without shortcuts.

Mining. Mining is a guessing game where your chance of winning is related to the how quickly your machine can perform calculations compared to how quickly other miners are performing similar calculations. Whoever guesses the right number first wins the right to add a new block of transactions to everyone’s blockchains, and does this by publishing this to the other computers on the network. Each computer performs a quick validation of the block, and they agree that the block and transactions conform to the rules, then they add the block to their own blockchain. Why does the miner do this? Because as part of the block, they get to award themselves with some amount of new bitcoins (currently 25 BTC, and halving roughly every 4 years, the next halving being July 2016). This block-adding happens roughly every 10 minutes on the network.

See a gentle introduction to bitcoin mining for further detail.

Due to this reward, bitcoin mining has got very competitive, with companies developing specialised hardware, called ASICs, which are very quick at the guessing game and associated number-crunching.

Bitcoin’s protocol and code ensures that it takes around 10 minutes for the network as a whole to guess correctly. This is the speed that transactions take to be confirmed onto the blockchain.

Slow for security. By making it slow (10 minutes is slow compared to how fast it could be down if the guessing game was removed), and by making it computationally and therefore financially expensive to participate in this process, it also makes it financially expensive for miscreants to buy enough processing power to write their own abnormal blocks of transactions into the blockchain.

Bear in mind that even if miscreants were to do this, all the other computers would need to agree with all of the transactions, so they still cannot insert transactions that break the business logic rules, eg conjuring bitcoins out of thin air.

Bitcoin security

There are two parts to this:

- Making payments

- Block control

Making payments. As discussed earlier, the only thing you need to make a bitcoin payment is the private key of the address you want to spend from. You need to balance making it hard for people to steal your keys, and having backups in case you lose your keys – there are stories of people throwing away old laptops containing – not bitcoins – but bitcoin private keys controlling bitcoins worth millions of dollars.

Block control. There are two parts to this. Firstly there is block-creation (“mining”), performed by some specialised nodes; secondly there is block validation, which is performed by all nodes. Like an army of independent accountants and auditors all auditing the same ledger, the vision of bitcoin is to have many thousands of independent block validators to be participating in keeping the system honest. This independence and mutual validation of transaction and blocks is supposed to prevent any one person or entity from adding rogue blocks and dominating the network with their influence.

However, in practice, miners join forces into ‘mining pools’ in order to win blocks more often. In a mining pool, one participant creates the candidate block, and the others get to work ‘mining’ it. If any of the participants wins, the spoils are shared with the pool. This has the effect of each participant getting paid out more often, but less amount, like a lottery syndicate. This smoothing of cashflow works well for paying back capital needed to buy mining equipment. As a consequence, the mining pool owners have greater power over the bitcoin network in terms of creating blocks, voting on protocol changes, and potentially re-writing recent ledger entries.

Without going into too much technical detail, if you have ability to re-write a recent block, then you could ‘unwind’ a payment in what is known as a ‘double spend’ attack. You would make a payment to a vendor, and have it confirmed in a block. If you can create a couple of blocks without the payment to the vendor, then the network will invoke the ‘longest chain rule’ and ignore / orphan the first block and use your longer chain instead. You also need to invalidate the original payment, by creating a slightly different transaction, spending the same bitcoins, but paying yourself or your friend, instead of the vendor. If you can slip this transaction into your new blocks, then the old transaction will be invalid to the network. Here’s an example. For more on the difficulties of changing the transaction list, read a gentle introduction to immutability of blockchains.

Your ability to do this shuffle increases with ‘mining power’, but it decreases with the age of the block you are trying to replace (the older the block, the harder it is to re-write), as each block ‘costs’ a certain amount of mining power to create, and you are competing against the rest of the network to create blocks.

Scams. It’s hard to write about bitcoin security without mentioning Mt Gox, an early bitcoin exchange. Bitcoin exchanges are websites you go to to buy or sell bitcoins. If you want to buy bitcoins, you first make a bank wire to the exchange’s bank account. When they sight the funds in their bank, they let you place orders to buy bitcoins from sellers. Likewise, sellers need to send bitcoins to the exchange’s bitcoin wallets before the exchange will let them sell the bitcoins. The exchange acts as escrow, holding onto cash and bitcoins and then releasing them once the trade has been made.

It is unknown what happened at Gox, but rumours include having private keys stolen, poor accounting practices, letting people trade first before sending collateral, etc. Just as you don’t blame the US Dollar if a Citibank branch gets held up and funds stolen, it wasn’t the security of the bitcoin network that was at fault; it was the security and poor practices of the exchange.

What is this decentralised bit?

Let’s go back to “Bitcoin is a decentralised digital currency”. We’ve seen that bitcoin is digital, and not really a currency (though it is easy to send, and it has a value that is determined by supply and demand on a number of exchanges). What about the decentralised bit?

Distributed validators. Centralised means one point or source of control, and decentralised is where control is shared among participants. In bitcoin, participants are the validators of the transactions and creators of blocks. If enough of them decide to play by different rules, then the others will need to follow suit. The validators have “voting power” proportional to how much computation power they have. Anyone can be validator, and get more votes, if they are prepared to pay for computing power, the costs of which are hardware, electricity, and support. So instead of one single authority who can change the rules, the rules can only be changed by consensus of those validators.

The validation logic (what does a valid transaction look like?) is baked into the code which is run by the validators.

Open source code. This code is open source, meaning that validators can see exactly what code or logic they are running. The version that is most often used (called the ‘reference implementation’) is stored here: https://github.com/bitcoin/bitcoin. In theory, anyone can contribute to this reference implementation by uploading changes, though there are gatekeepers, people, who have the final say about what gets included.

In theory, anyone can write versions of this software, so long as they conform to the technical and business protocols of bitcoin. For example you could write you own version of the software, but with cooler graphics, or a more user-friendly interface. If you want to change some of the protocol rules, however, you’d need to persuade the majority of the validators (miners) to run your software with the new rules. Here’s an example version that has some changes to the technical protocols: https://github.com/bitcoinxt/bitcoinxt

Changing the rules. So the rules can be changed, as long as you achieve majority consensus (another myth is that the limit of 21 million bitcoins cannot be changed. It can be changed, in one line of code, assuming you can get the majority of network participants to agree to run it). Getting the miners to agree to run code is the real challenge, as they have invested huge amounts of capital and will not readily agree to change anything which may harm their mining rewards – “The turkeys won’t vote for Christmas”.

Conclusion

You will probably have guessed by now that there is a lot more to bitcoin than I have been able to set out here. In giving a gentle introduction I have had to present some concepts at a high level, which in practice are complex and highly nuanced. But as you read and learn more on this blog I hope to be able to take you into a more detailed understanding of bitcoin, mining, digital tokens, and the underlying blockchain technologies…

Update: I have recently published a book, The Basics of Bitcoins and Blockchains which contains an updated version of this blog post and much, much more.

The Basics is an essential guide for anyone who needs to learn about cryptocurrencies, ICOs, and business blockchains. Written in plain English, it provides a balanced and hype-free grounding in the essential concepts behind the revolutionary technology. You can get “The Basics of Bitcoins and Blockchains” now on Amazon: https://amzn.to/2rNB1EQ

I’m confused. How come one transfers is instant but unconfirmed for 10 minutes until the miners approve it.

Transactions are broadcast instantly, and detected all over the network within seconds. However it takes time for the transaction to be bundled into a block, and mined.

Is the transaction considered valid before it is bundled into a block and mined? If yes, then what’s the point of mining it? If not then transactions are not instant.

The time is kind of arbitrary and relates to system security to prevent fraud.

Thanks for the article. Gradually I am putting this together in my head. But to me you glossed over several points.

1. How does the bitcoin originally get created? Who gets it first?

2. Who keeps track of what bitcoins I have, or is that determined by some unique bit coin key or identifier for each bitcoin? (Somebody got it first, then the ownership is traced through all the transactions?)

3. I’m really confused by the “address” and “private key” for a bit coin vs for a person who has the bitcoin? There must be two sets of addresses, one for people and one for the bitcoin.

I am not an expert in bitcoins, so what I am telling here might be wrong. If this is so, please would someone correct me!

1. Bitcoins are created “out of thin air” when a new valid block is created by a miner. The algorithm allows it that the miner adds a transaction which creates 12.5 bitcoins (as of today) out of nowhere and adds them to an own bitcoin address. This is similar as if the person who maintains the ledger would be allowed to add 10 bucks to his own account for every page completely filled out – but only exactly this amount! This new money comes from nowhere, and is just added to the complete worldwide amount of bitcoins.

2. The validating nodes must go back checking every transaction up to the first incoming transaction of this bitcoin address. It might have been a good idea to have something like a “backlink” for every transaction, pointing to the previous transaction of this address, however I do not know whether this really exists. Otherwise, the validator would have to check at least part of the whole 50GB completely.

3. There is no person “having” a bitcoin, since this is not a single physical item. This is in theory the same for ordinary bank accounts. Any person who has the access code to the bitcoin wallet or the bank account is able to spend the money. The notable difference here is that a traditional bank is forced by regulations to verify the identity of a person opening a bank account, for bitcoins there is AFAIK no such regulation. So, noone knows who is the legitimate owner of bitcoins in an address.

1. Yes. Technically “up to this amount” but in practice it is that amount.

2. Yes there is the concept of a backlink – transactions refer to previous transactions.

3. Theoretically yes but in practice there are ways to determine account owners. For example if you search Reddit for “tip” addresses people will display a bitcoin address which they claim as theirs.

Very good article about Bitcoin. Very clearly and easily explained about bitcoin. Thanks for sharing such information with us.