Confused by blockchains? Revolution vs Evolution

This article attempts to explain the difference between the revolutionary disruptive innovation of bitcoin and the evolutionary efficiency innovations of industry workflow tools, and why calling them both “blockchains”, even as a generic term, is incredibly confusing.

For the rest of this post, I will use the phrase “industry workflow tools” instead of industry blockchains, as some of the emerging solutions being proposed in this space are not blockchains (eg, R3’s Corda is not a blockchain but Digital Asset’s solutions are – however, both companies are proposing industry workflow tools).

Just as it’s not helpful to call Twitter and Microsoft Sharepoint “database companies” although they both use variations of databases, it’s not helpful to call cryptocurrencies, cryptocurrency companies, blockchain platforms and industry workflow tool companies “blockchain companies”, although this frequently happens in the popular press. Why? Because you don’t want to create misunderstandings like “But I thought you could only use 140 characters in Sharepoint.”.

To be clear, both cryptocurrencies and industry workflow tools both have admirable objectives in their own ways for their own purposes, as do both Twitter and Sharepoint.

Disruptive innovation: Public Cryptocurrencies

The purpose of bitcoin, according to Satoshi Nakamoto’s original whitepaper is to create “A purely peer-to-peer version of electronic cash [which] would allow online payments to be sent directly from one party to another without going through a financial institution“.

This is new and radically different to anything that has ever existed before. It is meant to enable:

- value to be held electronically without any third party being involved, and

- value to be transmitted without a specific third party being able to censor the transaction at will.

The problem statement is:

How do we use technology to create a financially inclusive system that anyone can participate in?

The proposed solution is:

Bitcoin

Efficiency innovation: Industry Workflow Tools

The purpose of successful incumbent institutions is to maintain and improve on their position by keeping customers happy, increasing revenues, reducing costs, becoming more efficient – ie to maintain a competitive, well-run business.

The problem statement is:

How do we use technology to improve our business and add shareholder value?

The proposed solution is:

Use industry workflow tools

These are incredibly different, more or less polarised problem statements, requiring incredibly different and targeted solutions. Blockchains have somehow been caught in the middle.

So why the conflation? Why are people confused about these entirely separate problems and solutions?

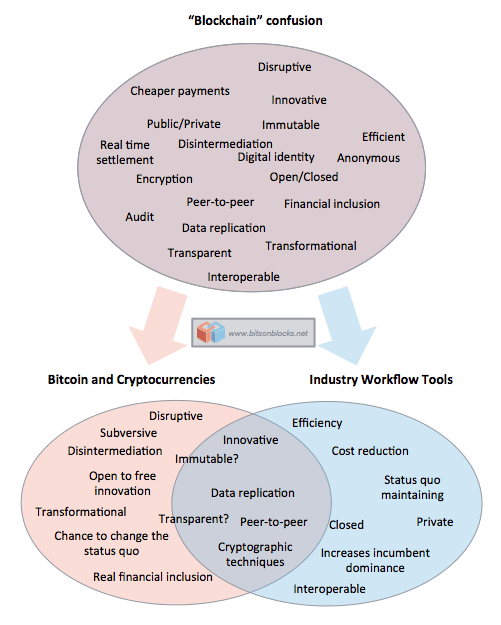

Somehow in all the hype and PR, industry workflow tools still seem to have retained some of the connotations of bitcoin, when industry workflow tools and cryptocurrencies have almost the opposite ideology!

Industry workflow tools and bitcoin are both separately exciting and innovative, but for very different reasons.

How did the confusion happen?

2013

In 2013 The ‘thing’ was bitcoin. No one really talked about “blockchain” apart from talking about bitcoin’s blockchain, ie the replicated ledger of all bitcoin transactions. It was called “the blockchain” because there was only one. (I am excluding the alt-coins like Litecoin, Dogecoin and other digital tokens as they only take up a tiny fraction of the mind-share of bitcoin).

2014

In 2014, because bitcoins were described as a new currency, the financial industry started to take notice. Bitcoins were pitched to the financial industry as an investment (buy bitcoins because the price will go up) and a trading asset (buy and sell bitcoins because you can make money) and a strategy (integrate bitcoin functionality because your customers will want it).

The financial services industry as a whole wasn’t interested in an anonymous, open, unregulated self-declared ‘currency’, backed by no government or central bank. They had no mandate to invest, and no framework to price it or understand it. Associations between bitcoins and scams, drugs and underground markets made the concept even less tasteful for traditional financial service industry participants. Even those who saw some potential were mostly put off by the small size and illiquidity of the market.

2015

In late 2014/15 the narrative moved away from bitcoins, towards blockchains and distributed ledgers (replicated ledgers without necessarily having chains of blocks). Institutions were saying “We’re not interested in bitcoin, but we are interested in the data-sharing technology behind it, the Blockchain”. In summary, “Bitcoin bad, blockchain good“.

The industry responded. In an attempt to garner interest, funding, customers, and higher company valuations, many bitcoin companies started rebranding as blockchain companies using more or less a text find-and-replace strategy (find the word ‘bitcoin’ and replace it with ‘blockchain’). This was also to avoid the negative connotations of the word ‘bitcoin’, and to participate in the interest in the word ‘blockchain’.

I have heard the phrase “we send it on/over/using blockchain” or “using blockchain technology” as a deliberate tactic not to use the word bitcoin, and to hide what is going on. This misleads customers, investors, and regulators. This deliberate misdirection is still currently pursued by some companies who use bitcoins, who assert that they are blockchain-powered when really they mean that they transfer value by buying, transferring, and selling bitcoins. One of the arguments is that by using the word blockchain instead of bitcoin, they attract less regulatory scrutiny and have a higher chance of opening a bank account, needed for fiat deposits.

This has hurt the industry by creating confusion, and in retrospect is incredibly short-sighted. This also hurt the companies who were genuinely using blockchain technology (not bitcoins) to attempt to solve other problems.

I call this The Blockchain Blunder.

Later, journalists, industry leaders, politicians, figureheads, consultants, bloggers and dinner party speakers started waving their hands and talking about “blockchain” (without ever specifying which one) being a solution for everything from disrupting banks to saving banks, from replacing 3rd parties to creating more efficient 3rd parties, and of course enabling financial inclusion. More pundits jumped on the bandwagon and regurgitated barely-researched content, creating the echo chamber of confusion. Chaos ensued.

Some technology vendors pivoted from bitcoin (not well paid) to industry workflow tools (better paid) and tried to retrofit iterations of bitcoin’s blockchain technology into perceived financial service problems, often without understanding the problems and the context of the financial service problems in the first place.

Incumbents in turn needed a ‘blockchain strategy’ and started doing proof of concepts by taking well known, well understood problems with well known, well understood solutions, and attempting to apply blockchain solutions to them. This makes sense if the purpose is to get hands dirty and explore the technology, though it doesn’t make sense from a pure IT architecture perspective.

This is where we stand in Q2 2016.

What has the effect been?

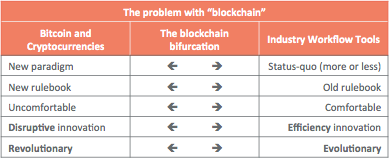

Bitcoin: a way for people to pay each other across the world without interference from financial institutions.

Industry workflow tools: mechanisms to share and update data between entities without a central point of control, creating efficiencies for incumbent industry participants.

By referring to these both as blockchains, the connotations have got jumbled up. Here’s how it should look:

Some benefits, reality checks, and points to consider

Now that we understand the difference between cryptocurrencies such as bitcoin, and industry workflow tools, let’s explore where the benefits lie.

Industry workflow tools will benefit incumbents

A shared or distributed ledger/fabric/communication tool/chat-app is only useful to business if it makes businesses better, more efficient, more competitive. The promise of the proposed industry workflow technologies is to join up participants and create a strategic advantage for them. The benefits of participation are potentially both cost reduction (cheaper IT) and oligopoly-consolidation (let’s maintain our advantage, together).

It’s a no-brainer for incumbent financial institutions to pursue what this technology can bring.

Industry workflow tools may benefit regulators

Regulators may want to insist on being able to ‘plug in’ to the workflow tools to get a better understanding of what is going on under their watch – something they have wanted to do for a long time. The transparency of asset ownership promised by industry workflow tools may have positive implications for systemic risk understanding and reduction.

However regulators should watch out for creating a new systemic risk – is something being created which is globally too big to fail? Are regulators enabling a monopoly or oligopoly?

Industry workflow tools may speed up asset settlement, but traders don’t want real-time gross settlement.

There is a difference between same-day settlement (T+0) and Real Time Gross Settlement.

Same day settlement

Same day settlement is beneficial to participants as it means that you get what you bought more quickly. Instead of waiting 3 days (T+3) to own your shares, the shares would be yours by the end of the same trading day (T+0). This frees up your pre-pledged collateral for use in another trade.

The technology to reduce the time taken to settle equities from T+3 to T+0 (ie 3 days to same-day) has been available ever since we have known how to edit a row in a database and tell someone else about it quickly. The Kuwait and Saudi exchanges operate on T+0 according to a member of NASDAQ staff.

It’s not the technology that has prevented the change, It’s the market structure, practices, regulation, and habits. The DTCC made this point clear in their blockchain whitepaper.

So if it’s T+0 settlement is not a technology problem, why will using newer technology help?

Real Time Gross Settlement

This is where trades are settled individually in as close to real time as possible, and there is no ‘netting’. Gross settlement means when I buy some shares one minute and sell them the next, we settle both trades in full (we don’t “settle the difference”).

However, netting is efficient. In real life you net wherever possible – for example if you buy your friend dinner, then later she buys you dinner, you wouldn’t insist that you pay each other back the full amounts on the restaurant bills – no, instead you settle the difference, ie ‘net’ them off against each other.

Market players don’t want real time gross settlement. Being able to trade in and out of positions during the day and only settle up at the end of the day provides a lot of benefit: having to settle every trade would reduce the fun that can be had and money to be made. It would also increase the amount of collateral that would need to be posted.

There is confusion between what bitcoin does (fairly real-time settlement of a BTC-denominated payment) and industry workflow tools being pitched as a solution to frictionless, real-time gross asset settlements (that traders don’t want).

Industry workflow tools may make innovation harder and more expensive

Unless built extremely carefully, a system affecting multiple participants could be harder to upgrade and could ossify more quickly than a system run by a single entity. If you think it’s hard to innovate a single banking app, just think how hard it will be to innovate one that touches multiple banks.

Who would coordinate it? Who bears the costs?

For analogy, the internet uses a couple of protocols called TCP/IP. There has been amazing stuff built on top. However, changing TCP/IP itself is incredibly hard, partly because there is so much software and firmware built on top of it.

What about the 3rd parties who were going to be disintermediated?

Today, 3rd parties set the rules and also enforce them, with some enjoying a quasi monopolistic status, and reaping the pricing benefits that that allows. With the industry utilities being built, the role of the 3rd parties may change a bit – they could become technology service centres and standards agencies. I don’t think they will be disintermediated.

Perhaps with these workflow tools, control and execution of the rules will lie with the participants (the banks running the nodes), and the 3rd parties will end up setting the rules and coordinating the upgrades: someone has to. Incumbent 3rd parties are shaping the narrative and working hard to make sure they remain relevant.

The promise of disintermediation is driven by bitcoin & cryptocurrency side, not from industry workflow tools.

Cryptocurrencies and Financial inclusion

The promise of bitcoin and its bag of technological tricks gave us for the first time in the history of the world a way for two online people anywhere on the planet to send value electronically without needing to onboard or rely on specific third parties. For or better or for worse, this is truly a step towards financial inclusion.

But here’s the rub: ask a policymaker what they want, they’ll say Financial Inclusion. Ask them what they don’t want, and many will say bitcoin: the most financially inclusive tool we have ever seen.

Bitcoin is the most financially inclusive technology that exists today. Industry workflow tools have no direct impact on financial inclusivity.

So what are next steps?

I am an incumbent, what should I do?

- Make best use of technology

- You should be using the best technology to increase revenues, reduce costs, increase efficiency, keep customers happy, and deliver profits to shareholders

- It’s important to use technology to remain competitive

- Get involved with industry workflow tools, or you might miss out!

- Defend against the disruptive innovation of cryptocurrencies

- Aside from political lobbying, the only defence against disruption is to get down and play on the disruptor’s terms. To compete with bitcoin you need to create an open, permissionless, censorship-resistant payment network that is better than bitcoin.

- That may be difficult to do while maintaining a banking licence

- Perhaps one long-term play might be investing in bitcoin firms (actual cryptocurrency firms, not ‘blockchain solution providers’)

I am interested in disrupting the financial industry, what should I do?

- Keep working on the public blockchains, the unprofitable stuff, the stuff that people are uncomfortable talking about

- Keep making the open networks better, solving the hard problems, proving the skeptics wrong

- Don’t lose focus: you are not trying to solve the incumbent industry’s problems. Industries aren’t disrupted by having better widgets built for them. Do you really need to dance with the devil?

- Don’t spend your VC money too quickly pre-empting traction. It will probably take longer than you think!

- You are trying to create a new way of doing things – for better or for worse, and however it may end up

Be careful what you enable.

I am sitting on the sidelines, what should I do?

- Keep reading, talking, learning, and understanding.

- Challenge the hand-wavers if something doesn’t sound or feel right

- Keep watching the evolution of this space, the future is exciting!

What does the future hold?

The disruptive innovators will keep working on bitcoin and variants, improving them, solving problems. Disruptive companies will come and go, the majority will fail.

The incumbents will keep working to remain competitive, keep their customers happy, and deliver profits to shareholders. They will ignore bitcoin because it’s not what they think their customers want, and the market is too small!

Then, when bitcoin or its progeny gets good enough, something will happen. Disruption is uncomfortable, it’s dirty, it’s subversive, it’s “Oh shit, we can’t do anything about this”. There will be intense lobbying and a concerted effort to ban or make the technology illegal. The technology will win. This is the story of disruption, which has been told over and over again.

The financial service providers in a cryptocurrency world will look very different to today.

Great post Anthony. Agree how incredibly frustrating and deceptive it is when bitcoin companies act as if bitcoin and ‘the’ blockchain are the same. I was recently speaking at a conference were the previous speaker was from a Bitcoin payments startup that shall remain unnamed. He said things such as ‘a blockchain payment costs $0.03’, ‘the blockchain has a market cap of $7bn’ etc. Awful.

I largely agree with the differentiation you are making. Although, I do think that in a few years we will see a convergence of the revolutionary public chain ideas and the more evolutionary business-process focused approach. But currently, your bimodal description is very accurate.

An excellent landscape shot, taken with the right amount of light and preparation. The thought of the incumbents (banks) taking on a service provision model is one I’ve read a few times now this year.

One thing you don’t really touch on though is trust and this where I see the bridge between the two camps you’re describing here. Banks inherently represent trust in our society and through that will be enablers for the rest of society to start using services built on top of Blockchain technology. As it becomes virtually invisible to the end consumer that this is what’s running under the hood, the benefits of crypto currencies and a more efficient use of capital will come to the fore.

This was a really good article. Bitcoin is surely here to disrupt things for good, as the reputation of institutions handling our money is on a downhill with regulators or governments always needing to nudge them or save them after a big debacle.

If the mainstream public starts to accept decentralised crypto through popular platforms via some kind of an incentive at the beginning, it will be a real game changer. For that, a much better version of bitcoin or ethereum is needed to address the bottlenecks.